IWG online meeting on state capitalism in the USSR.

DATE

April 22nd, 7 PM EST

WHERE

Online

CONTACT INFO

IG: @iwg.official | Twitter: @IWGOfficial | FB: @iwgusa | Email: us@leftcom.org

There is a lot of talk about the global recovery. In fact the figures suggest only a small rise in just a few sectors of production, while the rest of the economy is still trapped in the dead end of speculation. Meanwhile, world capitalism is taking a series of steps to solve the crisis ranging from quantitative easing to negative interest rates. In this unrelenting capitalist crisis, where the real economy is struggling to generate new wealth and where speculation continues to lead the way, finance dominates and continues to identify "safe" areas for financial assets. This dramatically reveals how speculation, a product of the crisis of a real economy choked by low rates of profit, continues to steer clear of production, thus compounding the risk of collapse of the global economic system

Those same analysts who previously did not spot the onset of the crisis much less recognise its causes, now tell us that the worst is over, that the crisis has passed and, with a bit of good will (read “more sacrifices by workers”), the future is as bright as a cloudless sky at sunset.

The international bourgeoisie has tried everything to get out of the devastating consequences of an economic crisis that it produced itself by exacerbating all the worst contradictions of the capitalist system. It is also true that, after putting millions of proletarians on the streets,[1] considerably reducing their already low social status and making the lack of jobs and increased exploitation for those who do work the only certainty in this world, the international bourgeoisie has again turned to finance to restart production which has been stagnant for over seven years. In short, they are trying to unblock the mechanism for producing surplus value by devaluing labour power and increasing the return on capital in "the real economy”. On the first front action was swift and deep (reduction of direct and indirect wages, higher taxes, less welfare, less job security and protection in the workplace, higher unemployment and intensified exploitation). However, on the second front their efforts have come to nothing, producing little or no result. Under capitalism’s inexorable economic mechanisms investment in the ‘real economy’ only happens if there is the prospect of capital gain, if reinvested profits can meet the need for valorisation (generation of new value) from the invested capital. If these prospects don’t exist, capital flies from the real economy. Investment thus does not take place and money is directed towards speculation, hoping to find the economic "yield" that the low returns from production no longer guarantee[2].

This is exactly what happened in the recent crisis. The low rates of profit pushed capital, especially American, to flee production and create asset bubbles. Once they burst the already fragile world economy was overwhelmed. For the analysts mentioned above this was stunning. For them and for all those like them, it became customary to use a pithy expression which Obama himself employed a lot in the aftermath of the crisis: “no more paper economy, no more chasing false mirages of speculation, we must return to the real economy.” But with the damage done and the capitalist economy stagnant, the question is what can convince capital to abandon the world of speculation for production? Simple, replies the US President in tune with the head of the Federal Reserve, followed by the usual retinue of analysts: by helping capital and those who manage it (Central Banks, banks of national importance, investment funds, insurance companies, financial institutions and lenders of every stripe) in every possible way to go back to being the driving force of the economy through massive state funding and regulatory incentives. No sooner said than done.

First in the US, then in Japan and lastly in the Eurozone, central banks began to support the financial sphere in its huge crisis of low liquidity and bad debts, with the removal of toxic products from their balance sheets thus balancing their books and favouring the recapitalisation of the largest banks. All this, of course, at the expense of the taxpayer. The next stage involved a drastic lowering of interest rates in order to reactivate credit channels which, in turn, should have led to a recovery of financial investment which would then trickle down to the entire economic system. Third, central banks started buying Treasury bills in order to furnish additional liquidity to the banks that usually held them. The aim was that these manoeuvres would increase the price of long-term bonds by reducing the yield and further restrict interest rate rises.

Whatever they say, the combined provisions of these three factors has produced poor results, in some cases almost nothing. In both the US and the euro zone, where the measures started late because they were "burdened" by political obstacles, the first wave of injections of fresh capital into banks did not bring the beginning of a recovery of loans to industry. On the contrary, the newly available finance served to swell greater speculation both in government overseas bonds, particularly attractive given their high rates of interest, and in the raw materials market led by oil before its price collapsed. This does not mean that no share of this capital went to the real economy, it means that only a small amount went there while business and personal interest rates remained very high, despite the very low cost of money. This left things essentially as they were. Continuing stagnation forced the Federal Reserve to accompany the measures taken with a further financial incentive that goes by the name of quantitative easing (QE). This is an indirect way for the central bank to create money, by issuing liquidity through open market operations initially in the financial system, with the hope that it then gets into the sphere of production of goods and services.

In the case of QE the central bank buys, for a predetermined and previously announced amount of capital, investments by banks such as stocks, bonds or securities of various kinds, especially those considered toxic, to positively improve their balance sheets. This is then used to buy government bonds, which usually takes place through special auctions. In reality, it is no different from the three measures that we have mentioned previously, only that the QE takes precedence over other financial interventions and is more direct and faster.

The Federal Reserve is also ahead of the ECB. From the beginning of the crisis until 2014, the American institution issued three “tranches”, shelling out the magnificent sum of $3500 billion to inject liquidity, to depreciate the dollar, and to reduce interest rates on Treasury bills in order to jump-start the economy and domestic demand. A "necessary" measure but one whose main aim in reality was to ensure that the dollar continued to be the leading global trading currency and to reinforce its role as a safe haven for speculators. In other words, the input of $3.5 trillion in the financial sphere was to aid the resumption of lending in the economy, but, above all, to "convince" the financial markets that the dollar remained the monetary "dominus" which the international economy cannot do without.

The ECB only followed in these footsteps in the second half of 2014, when the American experiment was already coming to a close. What has intense use of QE achieved? In the US, there has only been a partial recovery and serious social and economic problems remain. Meanwhile, the huge outflow of financial capital created by the Fed has resulted in a rise in state debt, which is officially close to 105%, an increase of 72%. For other analysts, not convinced by government "propaganda figures", it is nearer to 120%, because of billions outlaid by the Fed. It would be even higher, "thanks" to a series of unofficial hidden loans to second tier companies and banks which are not in the budget. Many states, especially those in the south, are facing bankruptcy and can only pay civil servants thanks to the raising of the federal debt ceiling by the Government. And speaking of debts, if you add private and public together, you would arrive at the astronomical percentage of 520% of GDP. This has resulted in the release of huge quantities of "greenbacks" which are now not worth the paper they are printed on. But this is only possible due to the fact that the US currency is backed by the strength of US imperialism.

This explains how, despite huge indebtedness at home and abroad, the US is able to impose the hegemony of the dollar on international money markets. It allows them to bring home billions of dollars in speculative investments on the dollar and on the US’ best economic assets. And yet this sort of speculation was behind the international crisis which created such huge deficits in the US that would put it among the countries at greatest risk even today. Only under these conditions have they been able, in the middle of the crisis between 2009 and 2013, to draw in $2510 billion from abroad compared with the $2600 billion printed by the Federal Reserve in the first two tranches of QE. Practically this means that so far the US hasn’t spent a cent on trying to revive its economy and restore the financial stability that was undermined by the bursting of the speculative bubble of subprime loans. In addition to China with $543 billion for the purchase of bonds, and Japan with $556bn, the major financiers of the US Federal debt are Brazil ($129bn), India ($60bn) and the UK ($32bn) plus another thousand billion dollars from about twenty smaller countries. This would not have been possible without the leading role of the dollar. Without it the US would not only be unable to amass this mountain of debt but would be at the point of no return.

Meanwhile, the US government boasts of a rise in the number of jobs that has reduced the unemployment rate to 5.4% on the basis of an unbelievable average monthly increase of 200,000 jobs per month. This is a complete lie. The figures mentioned above need to be set against jobs lost, since the figure of 200,000 refers only to jobs created from scratch and not the net figure resulting from the difference between the two. So there may be an increase but it will be much lower. In addition, it should be added that, for years now, hundreds of thousands of (former) workers have given up on finding a job and are not on any unemployment list. In other words they have completely disappeared from the statistics and, therefore, are no longer "unemployed". Another fact that refutes the much-trumpeted 5.4% is that those who are employed part-time, as seasonal workers or even workers who work for starvation wages for only a few weeks a year, are counted as employed workers. More than one American analyst has calculated that the real unemployment rate is above 15% and in the worst-case scenario could be almost 20%. Also according to these analysts, the current level of employment in the US is equal to what was in 1978 meaning that the crisis has taken us back to employment levels of nearly forty years ago.

As for the social impact of the crisis on income distribution, according to a survey from the University of California (Berkeley), after the costly injections of capital to the banks, 95% of the increases in income between 2009 and 2012 went into the pockets of the richest 1% of the population. The revenues of the remaining 99% stagnated or even declined. In fact, in the second half of the Sixties wages accounted for 51% of GDP. In 2007 they had already fallen to 45% and are currently at 42%. More than 46 million Americans are also surviving on charity. Charitable bodies provide meals and a minimum of primary care to those who need it and don’t have a penny to their name. So what little economic recovery we see is costing huge amounts of public funds, increasing social inequality, unemployment and greater exploitation of the working class as well as significantly accelerating the real process of pauperisation, in what is considered the most advanced example of Western capitalism.

Now it's our turn but without the power of the dollar

In the EU, after a few years delay, the same things have been done: lower interest rates, support for banks and then QE (by the end of 2014 for a total of slightly more than €1,100 billion) to sort out an economic situation that was not changing. The result? Apart from Germany, which has always been above the European average in economic competitiveness and commercial and financial capacity, and has managed to swim a bit better in the troubled waters of the crisis, nothing or next to nothing. A reform of the labour market that dates back ten years and the invention of the "mini job" or precarious jobs, paid a few Euros per hour, with fixed-term contracts that have given German capital an easily blackmailed, underpaid workforce has also helped. Government statistics which give comforting data on unemployment, even if they are nearly as false as the American figures, are also useful.

The Draghi recipe for QE has not had much effect even on weaker countries so far. Apart from Spain, which seems to be slowly recovering, again due to new labour laws which make Renzi's reform look like a joke, Italy, France, Greece and Portugal remain static. In Italy the long wished-for industrial recovery has not appeared, GDP has been declining for years and is now worryingly stationary with a slight blip upwards[3]. According to the latest figures (May 2015), state debt and unemployment, both youth and total, have further increased, despite the propaganda of the Renzi government. In the first quarter of this year industrial production was static, only certain export sectors have enabled GDP to go above 0.3%, due to the low cost of the dollar and the decline in oil prices. Apart from the motor industry, now showing some signs of life after suffering most in these long years of crisis, everything else is still in the swamp of stagnation.

So why, after the colossal amount of financial capital given to banks which brought interest rates close to zero, and after several crackdowns on pensions, wages and all the factors that lower the cost of labour power, is the capitalist machine still struggling to recover? For the simple reason that the rates of profit are still too low to justify investment. Because wages are still too high to justify creating new, real jobs. Because the companies themselves prefer to devote the greater portion of their investments to non-productive activities and limiting productive investment to bare essentials. And because the banks, despite rivers of capital flowing into their coffers at no cost, prefer not to risk the uncertain financing of businesses in crisis. With a weak market and low or falling industrial profits they are frightened they will again suffer as creditors. Better speculation, better the risk of returns that are "little and damned, but now" than the recently experienced bogeyman of becoming again that suffering long-term creditor of they which still bear the scars. And especially since the devaluation of the means of production and the cost of labour has not yet reached a low enough point to turn things round, the only premise for even a minimal economic recovery.

Negative interest rates

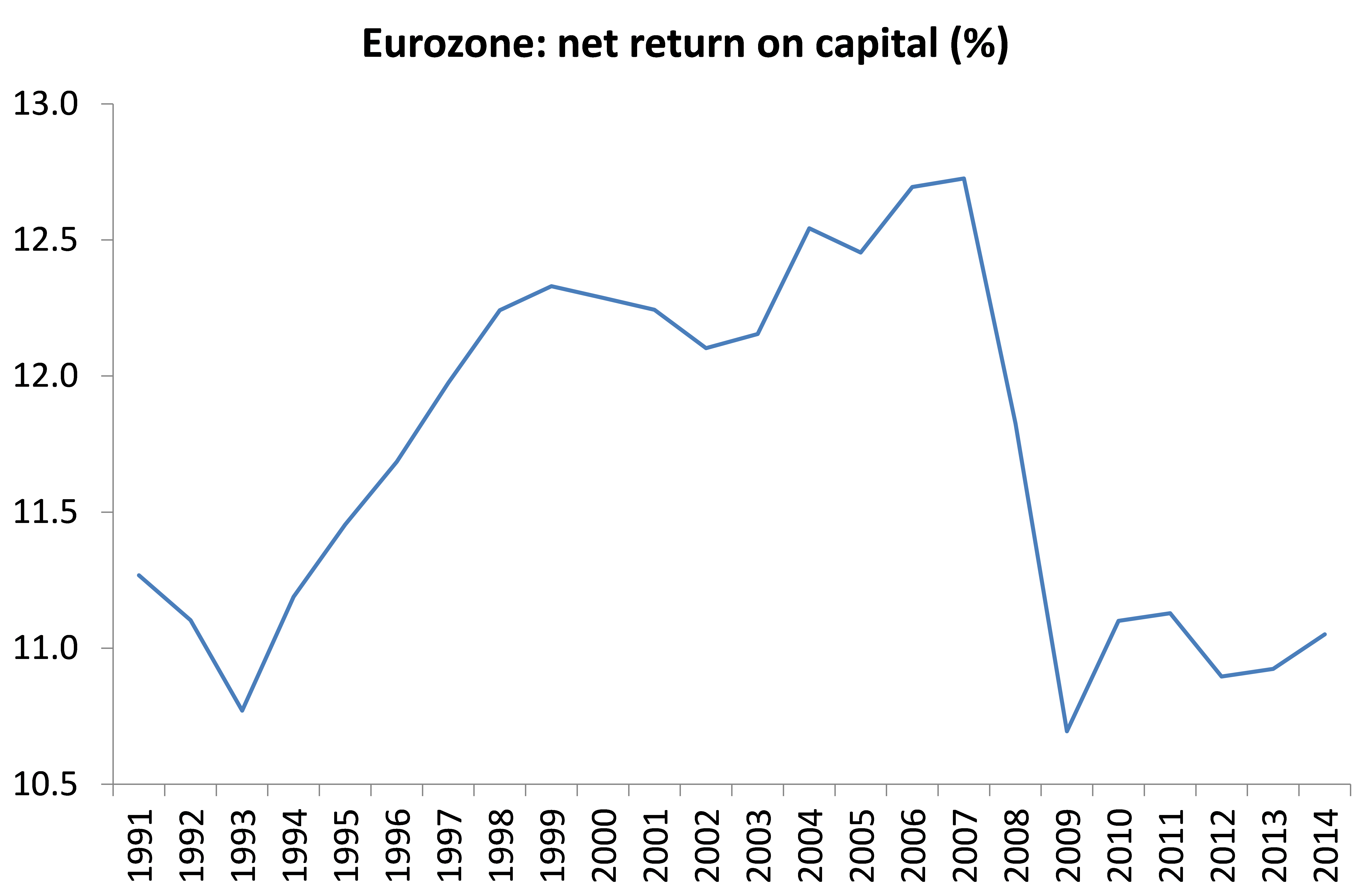

Before the outbreak of the latest crisis profit rates were insufficient to reward the capital invested. The market had already produced a growing separation between capital and production which, in its turn, generated a huge speculative mass, ready to move on any short term "deal" that it could in order to realise those profits that the sphere of real production made more and more difficult to obtain. Prior to August 2007, the "toxic cloud" of speculation was equal to 12 times the world GDP. Today, eight years later, world GDP has fallen by at least ten percentage units, while the "toxic cloud" has got bigger and, despite the efforts of governments and central banks, the reconnection of capital to production has not been achieved.[4] Banks fail to do banking, companies do not invest and the recovery is noticeable by its absence in almost every industry.

In continuation of this situation, as a bolt from the blue, on March 5 this year, the German Treasury auctioned a large amount of government bonds that, as usual, were immediately well-received by financial institutions. Everything was normal, except that the interest rates charged were not just low or very low, but negative. The German treasury offered to subscribers a bond rate equal to - 0.08%.

It is true that we live in a contradictory society, which works against social needs, as in the increase in productivity which, in the long run, triggers the falling rate of profit, thus challenging the very mechanism of capital valorisation. Increased labour productivity, instead of creating free time for workers, leads to greater exploitation, a lengthening of the working day and higher unemployment. Its the same with the development of the productive forces which, instead of creating more and better welfare, enriches only 10% of the population, while the remainder live between a halfway decent existence and the notorious poverty line. As "social progress" is combined with more and more job insecurity the dismantling of the welfare state is inversely proportional to the growing needs of the population from health to pensions. But having to pay to lend money to the state is the final straw. It looks like nonsense, an oxymoron. In reality everything that happens in capitalism, its contradictions and crises included, has its own very often perverse logic, which has its roots in the attempts of capital to ensure its survival.

Besides the distress which the crisis and the manoeuvres which the capitalists have subjected workers to they have three objectives in trying to restart the profit making machine.

In this way, depositing money in the bank is a cost rather than an investment, even if only with a minimum of return. For the same reason the Eurozone banks, which have to pay the European Central Bank to deposit their money, are discouraged from doing so, or at least that is the hope. Although only recently, the ECB has lowered its deposit rate to - 0.2% rate and no longer pays positive interest to other financial institutions thus immobilising their liquidity in its coffers. On the contrary it is the banks that must pay 0.2 to the ECB to keep their deposits. These latest financial resorts are amazing but real enough. However are they not just like propping up a shed teetering on one side which is in danger of another devastating collapse? Maybe. But one thing is for sure, the meaning of the ECB policy of negative rates is to discourage deposits and the purchase of government bonds and simultaneously to stimulate investment and, therefore, get the banks to finance the economy.

Since 19 January 2015 even the monthly interbank interest rate (Euribor) has fallen below zero. This is the first time it has ever happened. It is certainly an extraordinary situation, which has never happened before in Europe. Official interest rates which are normally used as a reference for mortgage costs and loans to companies are now in negative territory. These extreme manoeuvres are a symptom of a serious situation, so serious that not only are they struggling to jump-start the economy but their solution to the problem could be, according to many bourgeois analysts, the harbinger of a new economic catastrophe. In fact the owners of capital who are willing to pay a "fee" or "service" to the banks on their "savings" or, for banks when they buy Government bonds, very often do so in expectation of a return on their capital from speculation, and not from enfeebled production.

In fact, if the money was lent for productive activities, as the ECB would like, it would be a disadvantage for the banks themselves, because loans to the companies would run the gauntlet of current accounts, and would be deposited at the ECB itself and, therefore subject to taxation. The ECB introduced a tax of 0.2% a year ago once again with the aim of discouraging idle deposits in its coffers and to encourage lending to businesses. However instead of favouring expansion, the policy ended up playing a regressive role by forcing banks to find other solutions. At this stage two things are certain. The first is that loans for investment are taxed heavily making investment costly. The second is that in the current critical phase of the market, the risk is not worth the candle. That's another reason why the banks have every incentive to reduce their exposures and to give loans to business very sparingly. Much better to employ the capital in investment in sovereign bonds buying them from countries that still guarantee high interest rates or, at the even greater risk, to invest in the short term, in securities issued by governments in deep crisis. In order to receive funding from the ECB, the IMF or from speculation these states are forced to offer a high rate. In this case negative rates, instead of solving the problem of financing companies, may encourage its opposite, intensifying the speculation that continues to avoid production thus further hampering the much-talked about economic recovery.

Furthermore, if the policy of negative interest rates expands, a number of institutional investors notoriously less likely to take big risks such as insurance and pension funds faced with low or even negative returns to fund activities such as the payment of pensions and insurance payouts, would be forced to diversify their investments. The inevitable knee-jerk response is that they largely fill their portfolios with shares that are also at risk, albeit of a lower order. The low interest rates thus do not push capital towards productive investment but merely shift the axis of speculation from bank deposits and government bonds to the stock market. In conclusion: whether capital goes to high risk or lower risk speculation the scenario does not change much. We are faced with financial transactions that are unlikely to force capital to become productive.

In this perverse situation of the crisis of capitalism, where the real economy is struggling to produce new returns and where speculation continues to lead the way, financial asset management and the continuous identification of "safe" areas for finance, rules. This confirms with dramatic clarity just how the speculative stimulus, born of the crisis of the real economy choked by low rates of profit, continues to avoid production, compounding the risk of a collapse of the global economic system.

This does not mean that capitalism will destroy itself, but only that the measures adopted to overcome this "contingency" are few and very often ineffective. In order for the profit machine to start up again the necessary process of devaluation of capital goods and the cost of labour has to continue. Only when this devaluation hits rock bottom will they see a recovery in investment and production.

But it will only be a partial recovery within the limits set by the economic and financial crisis. This partial recovery will not be the beginning of a new cycle of accumulation, but only the tail-end of the old cycle where it will struggle more and more even to take small steps. According to the same bourgeois analysts, if all goes well, it will take twenty years for the global system to return to pre-crisis levels. Meanwhile, even more savage episodes of war will break out and there will be a further assault on the working and living conditions of the international proletariat. Against this ongoing and gradual economic and social barbarism, against its devastating consequences we have to put forward a social alternative to the way we produce and distribute wealth, outside and against the operations of capitalism, its crisis, its attempts to overcome it, against its profit system and exploitation.

Fabio *Damen*

Footnotes

[1] According to the International Labour Organisation (ILO) in 2013 the number of globally unemployed had risen to a new all-time record of 201.8 million people. The largest part of the group are the 74.5 million people aged 15–24.

[2] According to renegadeinc.com, “In 1970 ninety percent of financial flows were used to finance trade or investment in the real economy, only ten percent was speculative. Today more than ninety-nine per cent is purely speculative and has nothing to do with the real economy.”

[3] See Satyajit Das “Greek Problems mask the rising risks in Italy and France” Financial Times June 24 2015 which confirms that “Italy’s economy has shrunk 10% since 2007”. Unemployment is 12%, youth unemployment 44%, and government debt at €2.1 trillion is 132% of GDP.

[4] According to a Mckinsey Global Institute report. Debt and (Not Much) Deleveraging in February 2015 “Since 2007, global debt has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points”.

Journal of the Communist Workers’ Organisation -- Why not subscribe to get the articles whilst they are still current and help the struggle for a society free from exploitation, war and misery? Joint subscriptions to Revolutionary Perspectives (3 issues) and Aurora (our agitational bulletin - 4 issues) are £15 in the UK, €24 in Europe and $30 in the rest of the World.

The Internationalist Communist Tendency consists of (unsurprisingly!) not-for-profit organisations. We have no so-called “professional revolutionaries”, nor paid officials. Our sole funding comes from the subscriptions and donations of members and supporters. Anyone wishing to donate can now do so safely using the Paypal buttons below.

ICT publications are not copyrighted and we only ask that those who reproduce them acknowledge the original source (author and website leftcom.org). Purchasing any of the publications listed (see catalogue) can be done in two ways:

The CWO also offers subscriptions to Revolutionary Perspectives (3 issues) and Aurora (at least 4 issues):

Take out a supporter’s sub by adding £10 (€12) to each sum. This will give you priority mailings of Aurora and other free pamphlets as they are produced.

IWG online meeting on state capitalism in the USSR.

DATE

April 22nd, 7 PM EST

WHERE

Online

CONTACT INFO

IG: @iwg.official | Twitter: @IWGOfficial | FB: @iwgusa | Email: us@leftcom.org

This work is licensed under a Creative Commons Attribution 3.0 Unported License.

Comments

Having skimmed all the way through all the gory details of the convulsions of capitalism and arrived at the final paragraph in which we are urged to recommend an alternative way of running society, noting all sorts of theories from all and sundry politicos over the years, I come to a practical question ; How deep do air raid shelters need to be to be fully proof against blast, fire and radioactivity ?

Worry not T34. By the time the economic scenario of years of stagnation pans out and gets to that you [and I] will probably be gone anyway! And there is meanwhile also the prospect that the working class will reconstitute itself as the antithesis of a capitalism which has no option but to step up the attacks. Socialism or Barbarism remains the option.