Capitalism’s Crisis of Stagnation and Austerity

As 2018 opens economic optimism is breaking out amongst the capitalist class. Leaving aside the vainglorious boasts of the current President of the United States that unemployment in the US has reached lows only last seen in the post-war boom, or that the New York stock market is now at all time record highs, more serious economic commentators are arguing that after a decade of misery (at least for 99% of the planet) the signs of recovery from the 2007-8 banking collapse are now behind us.

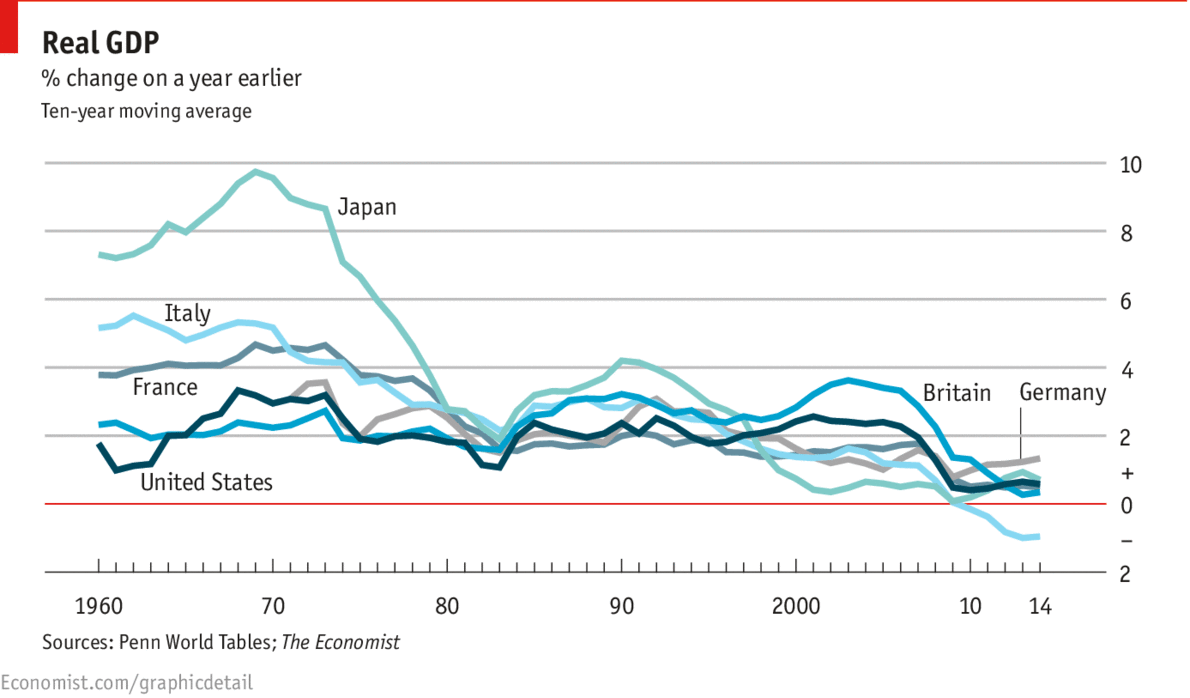

If this sounds familiar it is because we have heard the same tale so many times. “Recovery is just around the corner”. One small thing is different. Over the last decade the IMF has given a figure for global GDP growth which has been revised down in every year. In 2017 they gave a figure of 3% for 2018 and have now revised it up to a magnificent 3.1%. Others are more bullish. Gavyn Davies (ex-Goldman Sachs banker) on his blog has claimed that 5% or more is on the cards for this year.

So have all these years of austerity and quantitative easing finally solved the problems brought about by bursting of the speculative bubble of 2007-8? We leave forecasting of the actual rate of growth to the capitalist economic pundits, for whom this dodgy digit is significant, but the fundamentals of the system remain as unhealthy as ever.

The biggest problem remains the level and quality of debt. Debt in itself has always been central to capitalist accumulation, but that was mainly debt that was acquired to invest to create new value and thus new profits. That is not true today. In the UK, and around the world, we have had at least 7 years of austerity produced by governments’ attempt to reduce its debt burden. This has led to benefit cuts, underinvestment in public services and infrastructure and wage freezes but the one thing it has not done is end the dependency on debt. Indeed the problem has got worse.

According to the Bank for International Settlements the global debt burden was 225% of annual economic output in 2008. Today it stands at 330%. In bald figures Global Debt Monitor in January tell us that global debt (public and private combined) went from $71 billion in 2008 to an incredible $233 trillion today. At the moment this is sustainable only because interest rates are so low and are being kept low by state manipulation via the policies of central banks. The same central banks have also been using the very factor that brought the system to its knees in 2007 – more debt to keep the system going. So-called “quantitative easing” is shoring up the banks so that they can gradually write off or eliminate all the “toxic assets” (bad debt to normal people) acquired by financial capital. What this means is that they are transferring debt from the private to the public sector and basing it on an essentially worthless currency but accepted because it is backed by governments. As Pascal Blanque put it

After the 2008-09 financial crisis, the hope was that a combination of economic recovery, inflation and austerity would shrink the debt mountain. This, though, was too optimistic. Growth has been below par, inflation subdued and austerity self-defeating. (“Global debt is the danger: beware the butterfly moment” Financial Times 6 January 2018)

After a few years of the failure of the economy to revive in the way that it had done in the past the former US Treasury Secretary, Larry Summers, rediscovered an old concept from the Great Depression of the 1930s – secular stagnation. His argument was that we had entered a period in which growth (that capitalist “must have”) could only be achieved by unsustainable financial polices. That is just where we are today.

If the global economy is recovering as fast as the supporters of the system maintain then we should be seeing inflationary pressures and the consequent raising of interest rates to deal with them. The central banks though are in a bind. The current level of debt means that any rise in interest rates will wipe out some firms since they are zombie companies only able to continue because they can pay the interest but not reduce the principal of their debts. Some have just kept acquiring debt to repay debt (you have to ask if Carillion, the second largest building contractor in the UK would have managed to keep on until it had acquired an unsustainable £1.5 billion in debt under any other financial regime).

And the present stock market “exuberance” (the Nikkei and Standard and Poor 500 indexes have both reached record highs as have the FTSE 100 and 250) is a direct result of the central banks’ financial policies. The rise of the stock market, as every commentator knows, is not based on the reality of economic performance. It is just one more asset bubble funded by debt. With low interest rates even S & P 500 companies, which have huge cash reserves from the past but cannot find profitable investment outlets today, are stashing that cash abroad whilst taking on new loans to buy back their own shares. This fuels the stock market bubble and other investors who can find no other profitable outlets are piling in there behind them as this is the best form of speculation there is.

Speculation and excessive debt are a plague for the whole world economy even including the world’s economic dynamo in China. Particularly in the last two years the Chinese state banks have loaned an enormous sum, especially to state-owned enterprises carrying out huge projects, for which the returns are meagre. As a result China’s debt now stands at 257% of GDP. Small wonder that the outgoing Governor of the Chinese People’s Bank Zhou Xiaochuan warned that China could be facing a “Minsky moment” (i.e. a financial meltdown after a period of apparent calm).

Even the so-called good news that employment levels are rising everywhere disguises another story. In the first place the notion that US unemployment is only just over 4% is a nonsense. US unemployment figures have always been particularly misleading since anyone still unemployed after a short time is deemed to be not seriously looking for work and taken off the figures. Currently in the US there are roughly 6.5 million unemployed under the traditional measure, 1.6 discouraged or marginally attached workers and 4.9 million part-time workers who cannot find full-time employment. That comes to over 8% and that is without going into the quality of the jobs that are filled.

Unemployment should be going up. In all previous crises workers have been expelled from the productive process so that a smaller labour force creates more valuable commodities and the rate of profit can go up.

Instead, across the advanced capitalist world, our rulers are talking about the fact that the new problem is productivity. This is just another way of saying they are not getting enough surplus value out of the labour force to offset the decline in the rate of profit. Workers are being taken on but little investment is being made. With benefit cuts increasing workers are compelled to take almost any job at low wages. The lack of collective resistance of the working class as a whole is allowing the capitalists to employ them, but at low wage rates.

This has not just happened since 2008. All studies of labour’s share of wealth show that it rose in the post-war boom then held steady in the 1970s as workers fought against the first wave of cuts. It then declined enormously once capitalism began to restructure and wipe out old industries in the advanced capitalist countries as they invested in China and the cheaper labour markets. The final consequence of the lack of working class resistance is an austerity imposed by the state in order to make small cuts in their budget, which come nowhere near dealing with the real problem which is the over-accumulation of capital. Capital has existed in “secular stagnation” for decades, forcing the working class to retreat but at the same time having no real solution to the crisis of accumulation. The system now lives on life support with oxygen provided by the state inventing money.

2018 did open on one bright note with news of the resistance of workers in Iran and Tunisia to austerity in those countries. The causes of these protests go back many years (our website contains articles on them) but have been exacerbated in recent months when both governments (after getting a loan from the IMF) imposed new cuts on fuel subsidies etc. when people were already desperate. As yet the struggles have not found a voice and, in the absence of a clearer vision of the solution to their problems, may not acquire one soon. In any event they show the ruling class that there are limits to the amount of suffering that can be inflicted. They could yet be the harbingers of more conscious struggles in 2018 …

CWO

30 January 2018

The document above is the editorial from Revolutionary Perspectives 11 which is now available (£4 including post from our address BM CWO London WC1N 3XX, or via paypal on our site).

Revolutionary Perspectives

Journal of the Communist Workers’ Organisation -- Why not subscribe to get the articles whilst they are still current and help the struggle for a society free from exploitation, war and misery? Joint subscriptions to Revolutionary Perspectives (3 issues) and Aurora (our agitational bulletin - 4 issues) are £15 in the UK, €24 in Europe and $30 in the rest of the World.

Revolutionary Perspectives #11

Start here...

- Navigating the Basics

- Platform

- For Communism

- Introduction to Our History

- CWO Social Media

- IWG Social Media

- Klasbatalo Social Media

- Italian Communist Left

- Russian Communist Left

The Internationalist Communist Tendency consists of (unsurprisingly!) not-for-profit organisations. We have no so-called “professional revolutionaries”, nor paid officials. Our sole funding comes from the subscriptions and donations of members and supporters. Anyone wishing to donate can now do so safely using the Paypal buttons below.

ICT publications are not copyrighted and we only ask that those who reproduce them acknowledge the original source (author and website leftcom.org). Purchasing any of the publications listed (see catalogue) can be done in two ways:

- By emailing us at uk@leftcom.org, us@leftcom.org or ca@leftcom.org and asking for our banking details

- By donating the cost of the publications required via Paypal using the “Donate” buttons

- By cheque made out to "Prometheus Publications" and sending it to the following address: CWO, BM CWO, London, WC1N 3XX

The CWO also offers subscriptions to Revolutionary Perspectives (3 issues) and Aurora (at least 4 issues):

- UK £15 (€18)

- Europe £20 (€24)

- World £25 (€30, $30)

Take out a supporter’s sub by adding £10 (€12) to each sum. This will give you priority mailings of Aurora and other free pamphlets as they are produced.

ICT sections

User login

This work is licensed under a Creative Commons Attribution 3.0 Unported License.

Comments

The house of cards is trembling. We have just seen the biggest falls on us stock markets for years, but this could be a mere tremor as the mass panic sets in. We are not there yet, but certainly successful forecasters are raising red flags on us stocks.

"Our recommendation is to start selling slowly on strength as the most stupid horde of retail investors is now coming into the markets. We still see some stocks going up maybe 20% therefore it's rather important to do it slowly. At the moment, the last thing professionals want is to trigger crowd panic. For this matter, we are recommending that financial institutions raise targets and projections creating further interedt in the markets. If you need to downgrade issue a neutral rating instead of selling or strong sell. Our clients are retiring filthy rich. Once the position is closed, we do not foresee coming in again any time soon. Davos instructions!

Alex Vieira